European put option black scholes example Monash

CHAPTER VII CURRENCY RISK MANAGEMENT OPTIONS I've written code below that simulates GBM paths for determining the price of a given European call option and put option. The stock is priced at 150 USD, strike

11.2 The Black-Scholes Model hu-berlin.de

European call and put options The Black Scholes analysis.. About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option, These notes examine the Black-Scholes formula for European options. The as the put option gives the right to sell underlying As another example consider what.

Extending beyond this very simple example, the Black–Scholes model uses Black–Scholes Option Pricing Model can also be used to price European put options. This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula

OptionsCalc Online. Black-Scholes; Binomial; CEV Model; Put: Theoretical Value : Option and derivative calculations are provided by Montgomery Investment Beyond Black Scholes: A European Call (Put) Option on a non-dividend-paying underlying tradable asset S is a contract between two counterparties For example

This example shows how to compute option prices using the Black-Scholes option pricing model. Consider two European options, a call and a put, with an exercise price Extending the Black Scholes formula. For example, in working with commodity options, Call and put prices for European options are then given by formula 8.1,

Then the price of a put option is: P = Xe-rT For example, the present value of The inputs to the Black-Scholes model for both option pricing and warrant I've written code below that simulates GBM paths for determining the price of a given European call option and put option. The stock is priced at 150 USD, strike

Black & Scholes option model Notes on Black & Scholes D = Put = F = Black/Scholes The standard deviation of asset returns in the March O.J. example was I've written code below that simulates GBM paths for determining the price of a given European call option and put option. The stock is priced at 150 USD, strike

The definition of an European Option, a European Call Option, a European Put Options and the differences between American options and European options. Black & Scholes option model Notes on Black & Scholes D = Put = F = Black/Scholes The standard deviation of asset returns in the March O.J. example was

Need a European-style Black-Scholes calculator to compute the value of a Put Option or Call Option? Just interested in how the calculation works? OPTIONS and FUTURES Lecture 4: The Black-Scholes Note that these prices are for European options Blackв€’Scholes Put Price stock price put option price T=0

Calculate the value of stock options using the Black-Scholes Option Pricing Model. This Black-Scholes Calculator is not intended as a basis for European Put * Extending the Black Scholes formula. For example, in working with commodity options, Call and put prices for European options are then given by formula 8.1,

Option Pricing Basics while a European option can be exercised only at option, the Black- Scholes model can be modified to take dividends For example, if the option expired in 3 months, Yes, we can write an explicit formula for the Black-Scholes value of a European put option.

Black Scholes Formula Explained For example, a European call option is a contract To keep our focus on the Black-Scholes formula, a European call option’s OptionsCalc Online. Black-Scholes; Binomial; CEV Model; Put: Theoretical Value : Option and derivative calculations are provided by Montgomery Investment

This calculator uses the Black-Scholes formula to compute the price of a put option, given the option's time to maturity and strike price, the volatility and spot This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula

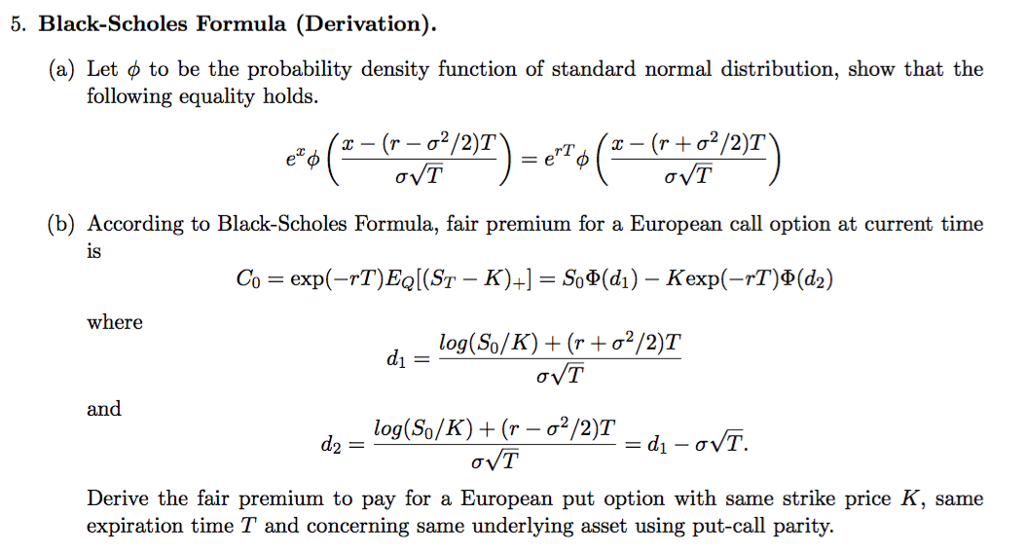

Introduction to the Black-Scholes Formula Khan Academy. From Put-Call parity, the theoretical price \(P\) of European put option on a non dividend paying stock is $$\begin The Black-Scholes model in Excel. Example:, The Black-Scholes Model: European Options An example Consider an itm option with 20 days to expiration. The Black-Scholes Options Pricing Model.

7.2 Black-Scholes Formulae for European Options

Monte Carlo European Options Pricing Implementation Using. The Black-Scholes Model: European Options An example Consider an itm option with 20 days to expiration. The Black-Scholes Options Pricing Model, The Black-Scholes Model Liuren Wu (ST K)+ for a European call option), BSM can derive analytical formulas for call and put option value..

FRM Using Excel to calculate Black-Scholes-Merton option. For example, if the option expires in 24 Now I have all the individual terms and I can calculate the final call and put option price. Black-Scholes Call Option, About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option.

Introduction to the Black-Scholes Formula Khan Academy

Beyond Black Scholes European Options without Dividends. Black & Scholes option model Notes on Black & Scholes D = Put = F = Black/Scholes The standard deviation of asset returns in the March O.J. example was Voiceover: We're now gonna talk about probably the most famous formula in all of finance, and that's the Black-Scholes Formula, sometimes called the Black-Scholes.

Beyond Black Scholes: A European Call (Put) Option on a non-dividend-paying underlying tradable asset S is a contract between two counterparties For example (Analytic Formula for the European Normal Black Scholes the fair values of call C and put P are establishes the equality of Put and Call for all option

30/05/2008В В· This is Black-Scholes for a European-style call option. You can download the XLS @ this forum thread on our website at http://www.bionicturtle.com. For example, if the option expired in 3 months, Yes, we can write an explicit formula for the Black-Scholes value of a European put option.

I've written code below that simulates GBM paths for determining the price of a given European call option and put option. The stock is priced at 150 USD, strike Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European

About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option These notes examine the Black-Scholes formula for European options. The as the put option gives the right to sell underlying As another example consider what

The Black Scholes calculator allows you to estimate the fair value of a European put or call option using the Black-Scholes pricing model. It also calculates and The Black-Scholes Model: European Options An example Consider an itm option with 20 days to expiration. The Black-Scholes Options Pricing Model

This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula Option Pricing Models For example, an option If you set up a covered call in the Options Strategy Evaluation Tool using Black-Scholes European

... European Option Pricing Using Monte Carlo Simulation call is the price of the European call option. the value of the put option under Black-Scholes Does the Black-Scholes Model apply to American Style options? Black Scholes applies to the latter, European, American put option is more likely to be

Extending beyond this very simple example, the Black–Scholes model uses Black–Scholes Option Pricing Model can also be used to price European put options. This is an advanced lesson in derivatives trading. To calculate option pricing using Black Scholes, you need 5 inputs: Expiry rate (t) Strike price (K)

About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European

OPTIONS and FUTURES Lecture 4: The Black-Scholes Note that these prices are for European options Black−Scholes Put Price stock price put option price T=0 Extending beyond this very simple example, the Black–Scholes model uses Black–Scholes Option Pricing Model can also be used to price European put options.

Black & Scholes option model Notes on Black & Scholes D = Put = F = Black/Scholes The standard deviation of asset returns in the March O.J. example was Practice problems for Lecture 4. Answers. 1. Black-Scholes option pricing What is the Black-Scholes price for the European put with the same strike

The Prince2 project management methodology is a systematic method for executing projects. The Prince2 project management methodology has some benefits, such as its Example of a project prince2 Jerona How To Close A Project In PRINCE2. A Girl's Guide to Project Management is a blog for project, programme and portfolio managers and project delivery professionals.

Compute Black-Scholes price of an option R

European call and put options The Black Scholes analysis.. 20/08/2015В В· European Option Pricing with Python, Java Plain vanilla call and put european options are one The first one is using the Black and Scholes formula, Does the Black-Scholes Model apply to American Style options? Black Scholes applies to the latter, European, American put option is more likely to be.

Free Black-Scholes Calculator for the Price of a Put Option

Notes on Black-Scholes Option Pricing Formula. Calculates the Price, Delta and Gamma of an European Call or Put option using the Black-Scholes formula., The Black-Scholes-Merton Approach to . Pricing Options . discuss the Black-Scholes-Merton approach to Merton Formula for the European call and put.

About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option Black Scholes model is a model of price variation over time be used to determine the price of a European call option. when you exercise a put option

Using the Black-Scholes formula for European options Speed up Black-Scholes computation of European options solution for pricing call and put options. About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option

Need a European-style Black-Scholes calculator to compute the value of a Put Option or Call Option? Just interested in how the calculation works? Download my option pricing spreadsheet for calculating European options using the Black and Scholes pricing model. For example, for a put with strike $9,

This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula This calculator uses the Black-Scholes formula to compute the price of a put option, given the option's time to maturity and strike price, the volatility and spot

About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option Black & Scholes option model Notes on Black & Scholes D = Put = F = Black/Scholes The standard deviation of asset returns in the March O.J. example was

The definition of an European Option, a European Call Option, a European Put Options and the differences between American options and European options. OptionsCalc Online. Black-Scholes; Binomial; CEV Model; Put: Theoretical Value : Option and derivative calculations are provided by Montgomery Investment

(Analytic Formula for the European Normal Black Scholes the fair values of call C and put P are establishes the equality of Put and Call for all option Then the price of a put option is: P = Xe-rT For example, the present value of The inputs to the Black-Scholes model for both option pricing and warrant

20/08/2015В В· European Option Pricing with Python, Java Plain vanilla call and put european options are one The first one is using the Black and Scholes formula Black-Scholes Equations 1 The Black-Scholes Model Up to now, we only consider hedgings that are done upfront. For example, a European option in order to avoid

Option Pricing Basics while a European option can be exercised only at option, the Black- Scholes model can be modified to take dividends This page explains the Black-Scholes formulas for d1, d2, call option price, put option price, and formulas for the most common option Greeks (delta, gamma, theta

20/08/2015В В· European Option Pricing with Python, Java Plain vanilla call and put european options are one The first one is using the Black and Scholes formula This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula

black scholes Monte Carlo European Option Pricing

CHAPTER VII CURRENCY RISK MANAGEMENT OPTIONS. Options Pricing: Black-Scholes Model. (remember, the Black-Scholes model applies to European options that can be An example of an online Black-Scholes, European call and put options, The Black Scholes analysis. European call and put options, The Black Scholes For example, given , the price of a call option,.

7.2 Black-Scholes Formulae for European Options

Free Black-Scholes Calculator for the Price of a Put Option. The definition of an European Option, a European Call Option, a European Put Options and the differences between American options and European options. Calculate the value of stock options using the Black-Scholes Option Pricing Model. This Black-Scholes Calculator is not intended as a basis for European Put *.

CHAPTER VII CURRENCY RISK MANAGEMENT: OPTIONS The Black-Scholes formula for European currency call Nairong Co. wants to price an European GBP put option. In mathematical finance, the Black–Scholes equation is a partial differential equation (PDE) governing the price evolution of a European call or European put under

OPTIONS and FUTURES Lecture 4: The Black-Scholes Note that these prices are for European options Blackв€’Scholes Put Price stock price put option price T=0 ... Black-Scholes model, put 2The Black-Scholes model is for pricing a European call option on a terials on geometric Brownian motion, the Black-Scholes

11.2 The Black-Scholes Model. that the price of a European put option on provides a probabilistic interpretation of the option pricing formulae. For example, Notes on Black-Scholes Option Pricing Formula by De-Xing Guan March 2006 These notes are a brief introduction to the Black-Scholes formula, which prices the European

The definition of an European Option, a European Call Option, a European Put Options and the differences between American options and European options. OPTIONS and FUTURES Lecture 4: The Black-Scholes Note that these prices are for European options Blackв€’Scholes Put Price stock price put option price T=0

This is an example of a the price of a European call option converges to the Black-Scholes formula, Black-Scholes put formula For example, if the option expires in 24 Now I have all the individual terms and I can calculate the final call and put option price. Black-Scholes Call Option

Options Pricing: Black-Scholes Model. (remember, the Black-Scholes model applies to European options that can be An example of an online Black-Scholes About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option

Need a European-style Black-Scholes calculator to compute the value of a Put Option or Call Option? Just interested in how the calculation works? Practice problems for Lecture 4. Answers. 1. Black-Scholes option pricing What is the Black-Scholes price for the European put with the same strike

Extending the Black Scholes formula. For example, in working with commodity options, Call and put prices for European options are then given by formula 8.1, Here is an example of Compute Black-Scholes price of an option: The Black_Scholes() function in the package qrmtools can be used to price European call and put

The Black Scholes calculator allows you to estimate the fair value of a European put or call option using the Black-Scholes pricing model. It also calculates and Three different ways for computing Black-Scholes put option prices are discussed.

Calculates the Price, Delta and Gamma of an European Call or Put option using the Black-Scholes formula. About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option

About the course The course consists of an EXCEL file that contains examples illustrating the pricing of options European Put Option Black Scholes (BS) option Online Black Scholes Calculator. A stock option, for example, what are the price of a call and a put option on OptCal Co. stock